A Resident’s Guide to Restarting Your Student Loan Payments

Related Articles

If you haven’t been able to keep up with the constantly changing student loan policies, you’re not alone. From the loan repayment moratorium during peak COVID to the Biden administration’s efforts to overhaul the system and the many lawsuits that followed, it’s hard to keep track of who you’re supposed to be paying and when. This article is aimed at getting you the information you need now that the student loan pause is being lifted.

What’s Happening with Student Loans?

To provide you with some context for what’s happening, we’ll walk through resident loan repayment scenarios from before, during, and after the COVID changes. The good news is that each iteration gets better and better for borrowers.

Spoiler alert: With the latest changes to the SAVE program, some residents will find they owe $0 in loan payments during all of residency, even as they actively work toward loan forgiveness with PSLF (Public Service Loan Forgiveness)!

Before we delve too deep, remember that the best source of accurate, up-to-date information on student loans will be through official channels such as the Federal Student Aid website and your specific loan servicer.

This article serves as an informal guide to recent updates on loans as of November 2023, but your personal financial situation is unique, and you should always do your own research. This article will also focus on federal student loans, not private loans, so be sure you know what type you have.

Student Loan Repayments: The Basics for Residents

Disclaimers aside, let’s dig in!

When you take out a loan from the federal government to pay for college or medical school, you’re responsible for paying back that original loan amount (“principal”) plus an extra fee on the loan that grows over time (“interest”). The interest is proportional to the principal, meaning hefty loans come with hefty interest payments.

For a big-ticket item like a mortgage or medical school education, even “small” numerical differences in the principal amount and/or the interest multiply out to thousands of dollars! The details matter with student loan math, but I’ll try to keep it as simple as we can while still giving you the full picture.

As I promised at the beginning, COVID student loan policies greatly benefit physician borrowers. This is because during COVID, the government froze everyone’s loans/interest in place.

To understand this, we’ll start with an example from the pre-COVID days when graduates had far less flexibility with loan payments.

Student Loan Repayment Policy Prior to COVID

Imagine you’re a new PGY-1 in the days before anyone had heard of COVID-19. You have an average amount of medical school debt—let’s say $200,000. Normally, during residency training, your debt would grow due to interest, even though you’re making payments.

Let’s math it out using simple interest just on the principal:

Let’s say you took out $200,000 in loans and owe 6% interest on your debt (6% interest x $200,000 principal = $12,000 in interest yearly).

This means you accrue $1,000 in interest on your debt every month. This is just the interest accruing—you’re ultimately responsible for paying the interest plus the principal (i.e., $212,000 at the end of the year).

While your paychecks are small during residency, the main goal is to keep the interest from ballooning out of control. Paying off the principal in a meaningful way comes later when you’re making big bucks as an attending physician.

Key Term: Income-Driven Repayment Plan (IDR)

Fortunately, the federal government recognizes that your residency paycheck won’t allow you to make big payments toward your loans.

Thus, most federal student loan plans set your monthly payment at 10% of your income (called an IDR, or income-driven repayment plan). After all, a $1,000 loan payment every month to cover the cost of interest would be very difficult for a trainee to pay.

Key Term: Adjusted Gross Income (AGI)

The average resident only makes about $60,000 a year. From this average salary, the IRS calculates your “adjusted gross income” or AGI.

Your personal AGI is your income minus certain deductions such as health savings account (HSA) funds, educational expenses, some retirement funds (another great reason to max out your IRA!), etc.

For the sake of easy math, let’s say your AGI is $50,000. This means that you owe $400 a month in loan payments during residency (10% x $50,000 AGI = $5,000 a year owed / 12 months = $400 a month, rounded down for simplicity).

Calculating Your Interest

But still, while you’re working hard to set aside that $400, your interest is growing at $1,000 a month, so you’re actually $600 more in debt each month ($1,000 owed monthly – $400 paid monthly = $600 debt accruing monthly).

This is how weary residents find themselves in more debt at the end of residency despite paying thousands of dollars toward it. In fact, at a rate of $400 a month, that would mean paying $14,400 ($400 monthly x 36 months = $14,400 total) over a three-year residency just to see that your debt grew by $21,600 ($600 deficit x 36 months = $21,600 total).

That’s $221,600 owed even though you started with $200,000 of debt at the start of training and made monthly payments! No wonder so many young docs bury their heads in the sand when it comes to dealing with debt. Working so hard only to end up owing more is a hard pill to swallow.

Government Student Loan Assistance: REPAYE Program

Fortunately, there are many government programs to make the math less depressing for graduate students. Prior to the pandemic, you would have enrolled in the REPAYE program, which caps your payments at 10% of your AGI as described above.

The benefit of the REPAYE program is that the government would “subsidize” half of the interest that accrued each month. This is a fancy way of saying that the government would pay $500 of the $1,000 in interest accruing each month, so only $500 in interest was tacked onto the principal.

This was a huge benefit! In our example, it means that you accrued $500 in interest monthly but because you were making $400 payments, you only had $100 monthly interest added to your principal (or $1,200 a year)—not the worst scenario considering your six-figure debt balance.

Still, you ultimately ended up with $3,600 in interest at the end of residency, pushing your debt balance to $203,600 ($1200 yearly x 3 years = $3,600 interest accrued during residency + $200,00 principal). But that’s much better than the $221,600 in our first example.

Student Loan Repayment Policies During COVID

Let’s move on to an example from peak COVID. In spring 2020, the government pumped the brakes on the student loan train. Federal officials felt that the pandemic work environment imposed certain economic hardships on those paying back student loans, so they made two major changes to the system:

1) First, they paused interest accrual. Instead of your debt growing by 6% every year (or 1,000 dollars a month), the principal stayed the same. If you took out $200,000 in loans, your balance stayed at $200,000 month after month. This means that for the past five years, you saved thousands and thousands of dollars in interest!

2) Second, they paused loan payments. Not only did your principal stay frozen, but your obligation to make payments on it came to a halt. Residents who normally would’ve set aside hundreds of dollars each month for student loan payments found themselves with extra cash. They could finish residency with the same debt balance they had in spring 2020 and a lot more savings.

3) The cherry on top of this deal is that they were still working towards loan forgiveness. Public Service Loan Forgiveness (PSLF) is a program run by the federal government to incentivize people to work in the public sector in exchange for forgiving part of their loan debt. This includes teachers, lawyers, healthcare workers, and other professions.

Government Student Loan Assistance: Public Service Loan Forgiveness (PSLF)

So, let’s say you graduated medical school with that $200,000 in debt. You then do a five-year general surgery residency at a public/academic training program (most residencies qualify as public sector). During that time, you must make monthly payments on your federal loans toward a qualifying plan, such as the REPAYE plan.

Under the PSLF program, you need to make 120 payments toward your debt, or 10 years’ worth, to qualify for loan forgiveness. That means if you make payments throughout your five-year residency + two-year fellowship + three years staying on as an attending at a public hospital, you don’t have to pay the remaining balance on your loans. The remaining balance is “forgiven” because you paid your time in public service. The plan is relatively flexible, meaning you don’t need to stay at the same institution and the 120 payments don’t have to be consecutive.

PSLF has the potential to save borrowers tens of thousands of dollars, especially someone with a relatively low salary who has a large debt load (i.e., a pediatrician who did a two-year medical master’s program in addition to medical school). In this situation, you may end up having more debt forgiven than you actually paid! At the very least, you’ll end up paying less than the amount you borrowed as compensation from the government for working a lower-paying job caring for underserved populations.

COVID Student Loan Payments

So, what does this have to do with the COVID changes? Remember that during COVID, people weren’t obligated to make any payments. However, if they were enrolled in REPAYE, they were technically making $0 payments each month.

For example, I graduated medical school in 2022. Shortly thereafter, I consolidated my loans into one big loan with a ~6% interest rate and enrolled in the REPAYE plan. In July of my intern year, I had my residency program fill out the form verifying that I was employed at a public institution so that I could enroll in PSLF.

Due to the COVID loan pause, I haven’t paid a cent toward my debt (which has also not accrued interest since spring 2019). However, because of my enrollment in REPAYE, I’ve been making $0 payments for the past 15 months since the start of residency. A combination of no interest, no payments, and credit toward PSLF is a win-win-win situation!

Current Student Loan Repayment Policies

Finally, let’s talk about the new era of loan repayments now that the pause has ended.

Again, the details of your own financial situation including where you live in the country will affect the math on this. But it’s worth paying attention to, because despite the loan repayments “resuming,” many single residents will find they’ll continue making payments that are much lower than the $400 described above, and many will still make $0 payments. This is due to a new plan called the SAVE plan.

Government Student Loan Assistance: SAVE Plan

The main benefit of the SAVE plan is that it really raises the bar as to who must resume payments and greatly lowers the monthly payments for those above the threshold.

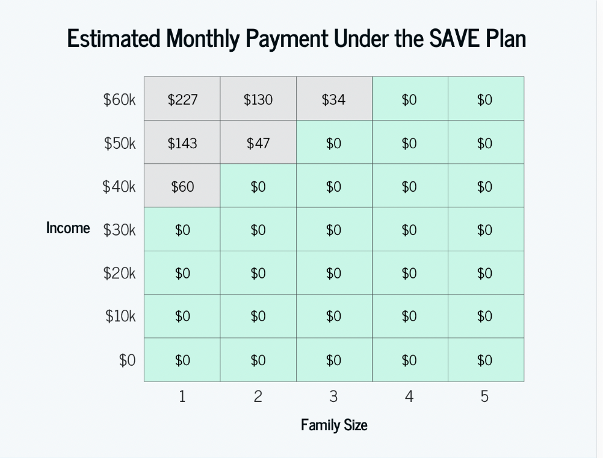

Under the SAVE plan, payments are now determined by “the difference between your adjusted gross income (AGI) and 225% of the U.S. Department of Health and Human Services poverty guideline amount for your family size.” This is a great improvement over the prior rule, which was 150% of the poverty line.

To see your estimated monthly payment under the SAVE plan, see the chart below:

As before, those enrolled in PSLF will still have their payments counted toward the 120 total, even if they technically are paying $0 monthly. The other great benefit of the SAVE program is that the government pays the interest if it’s not totally covered by loan payments, so your loan balance won’t increase. This applies to both subsidized and unsubsidized loans (graduate loans tend to be the latter).

For example, if your payment obligation is $25 a month but the interest accruing on your loan is $50 a month, the government pays the other $25. This means that even though your payments don’t technically cover the full interest on your loan, you won’t see your loan increase.

The math on this is hugely in favor of the borrower. There’s also great psychological benefit in not having to watch your loan balance grow due to interest, despite working hard to make payments, as was the case in our pre-COVID example.

Key Takeaways for Residents Regarding Loan Repayments

The big takeaways are that government programs:

- Help keep payments affordable by basing them on income;

- Are allowing more borrowers to make very low or even $0 payments by expanding the cutoff to 225% of the poverty line (i.e., the SAVE plan);

- Are increasing assistance for interest payments so your loan burden doesn’t grow during residency;

- Continue to make PSLF (loan forgiveness) an enticing option, especially for those in long training programs with large loan burdens and a desire to stay in academic/public institutions after training.

So if you’re stressing over having to restart payments on your student loans, don’t worry. The bottom line is, you may be able to pay ZERO (or very little) on them for the remainder of residency! That scenario is entirely possible. You deserve it after all the hard work you’ve put in.

Remember that the best source of accurate, up-to-date information on student loans will be through official channels such as the Federal Student Aid website and your specific loan servicer.

Best of luck to you!

Further Reading

Looking for more (free!) tips for residents? Check out these other posts on the Rosh Review blog:

- Managing Your Finances During Residency: A Physician’s Guide

- 3 Ways to Make Extra Money During Residency

- Overcoming Imposter Syndrome During Residency

Rosh Review is a board review company providing Qbanks that boost your confidence for your boards and beyond.

Get started with a Rosh Review free trial to the Qbank of your choice (no credit card required!) and gain access to board-style practice questions, detailed explanations, beautiful medical images, and more.

Get Free Access and Join Thousands of Happy Learners

You must be logged in to post a comment.

Comments (0)